{kind=link}

By: Steven E. Zeller CFP, CExP, AIF

Like most business owners, you’re likely exploring ways to strategically grow your revenue, increase profits, and minimize taxes. This is a common goal. As your cash flows increase, you may find yourself seeking ways to reduce your growing tax burden. Often, we explore sensible capital expenditures or business reinvestments that align with your strategic goals, which is a healthy exercise.

But sometimes, business owners could benefit from strategies to accumulate personal assets and reduce taxes. Depending on specific criteria, a Cash Balance Plan could be a powerful tool to achieve this objective and significantly reduce your tax burden.

What is a Cash Balance Plan? It’s an ERISA-based hybrid plan, a unique blend of a Defined Benefit Plan and a Money Purchase Plan. To plan participants, it resembles a Defined Contribution Plan, like a 401(k), but the IRS treats it as a Defined Benefit Plan. This plan operates alongside your 401(k)/ Profit Sharing Plan, offering an additional tax-deferral strategy for accumulating retirement assets.

Cash Balance Plans are effective tax-qualified retirement funding vehicles designed to help business owners aggressively accumulate retirement assets. They are beneficial if they have fallen behind in their retirement savings goals.

Like a Money Purchase Plan, a Cash Balance Plan has fixed contributions for each participant each year. Additionally, plan participants receive interest credits based on the established interest rate defined in the plan. Often viewed as a feature of flexibility, an increase or a decrease in the value of the investments within the plan does not affect the benefits promised to the participants. Gains and losses from the plan’s investments reduce or increase the plan sponsors contributions. The employer oversees the risk/reward design of the investments with the assistance of a professional investment advisor. A portfolio is designed for reasonable and relatively stable long-term growth.

Here are some itemized potential benefits for the business owner:

- Significant tax savings. The funds contributed to the plan in the first year of implementation are tax-deductible and considered an ” above-the-line” deduction. Also, employees with high earnings may be able to accelerate their savings. Administration fees may be tax-deductible.

- Protection of assets from creditors. The Cash Balance Plan is a tax-qualified ERISA plan, so it is protected from creditors.

- The plan can help attract and retain valued employees. Many younger employees may find an employer-funded retirement plan attractive.

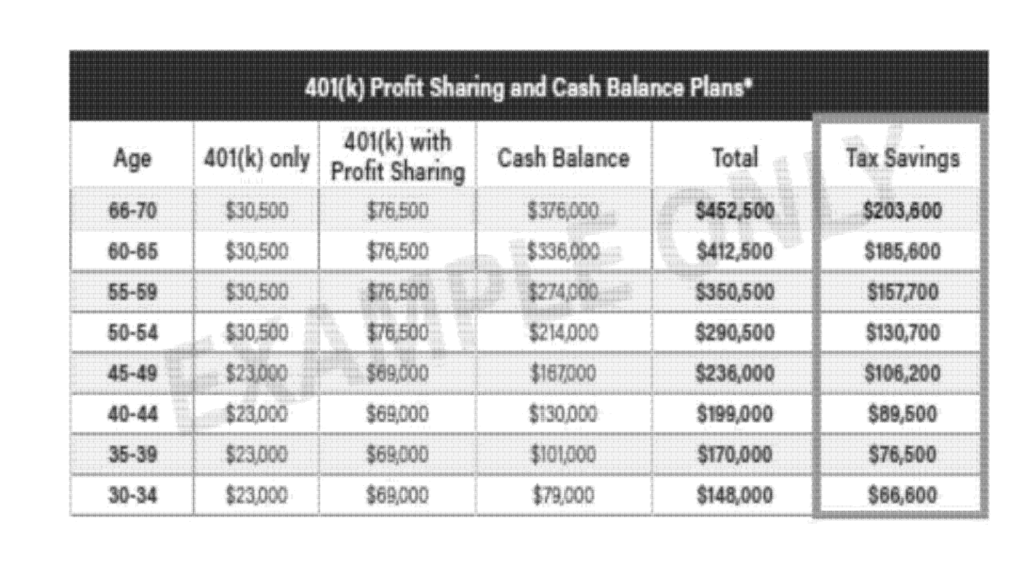

- Cash Balance Plans can help business owners accelerate their retirement savings. In 2024, the potential contribution to a Cash balance plan can be $376,000 (for participants aged 66 -70 and in a top income bracket). See the table below for contribution limits and potential tax savings.

Below is a table that illustrates the maximum contribution for a 401(k) based on age, along with the profit sharing and potential contribution of the Cash Balance Plan. The CB contribution is based on age and income.

Source: Cash Balance 101: FuturePlan by Ascensus

Assets in the plan are not allocated into separate accounts for the participants, and the participants cannot direct the investments within the plan. The investments and contributions are in a pooled fund managed by the Trustees.

One of the unique features of a Cash Balance Plan is its age-discriminatory aspect. The older the business owner, the more income they can allocate to the plan pre-tax. Conversely, the younger the other plan participants (employees), the lower the contribution requirements are to the sponsor (owner). This makes it ideal for a company where the owner is considerably older than the other plan participants, especially if the owner is in their 50s or older.

Another ideal scenario for a Cash Balance Plan is when the owner’s or potential income is significantly higher than the other employees. This income disparity is a key factor in the plan’s effectiveness and should be considered when evaluating its suitability for your business. Some requirements must be met. The CB plan can be implemented if the annual non-discrimination requirements are satisfied. At a minimum, a CB plan is required to cover 40% of employees or 50 employees, whichever is less.

Some owners look for ways to increase their cash flow to help fund a Cash Balance Plan, such as R&D Tax Credits, Employee Retention Credits, etc. However, these need to be vetted by a tax credit specialist, and current laws and eligibility must be followed carefully. But suppose the conditions are suitable for the owner. In that case, they are interested in saving on taxes and accelerating retirement savings, and it helps retain employees; it might make sense to perform an employee census-based analysis.

If you are a business owner interested in having an advisor work with you on an analysis or have any questions regarding Cash Balance Plans, feel free to contact me at szeller@zellerkern.com .

The financial consultants of Zeller Kern are registered representatives and investment adviser representatives with and offer securities and advisory services through Commonwealth Financial Network, Member FINRA/SIPC, a registered investment adviser. Financial planning services and fixed insurance products and services offered by Zeller Kern Wealth Advisors, a registered investment adviser, are separate and unrelated to Commonwealth. Zeller Kern Wealth Advisors, 2237 Gold Meadow Way, Suite 100, Gold River, CA 95670, 916-436-8270. Zeller Kern does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation. This material is not intended to replace the advice of a qualified tax advisor, attorney, or accountant. Consultation with the appropriate professional should be done before any financial commitments

regarding the issues related to the situations above are made.

Connect With Steve